Since we first published our analysis of India's economic recovery from COVID back in September the leading indicators have shown continuous improvement. As we enter India's all-important festival season we take an updated look at the data and find renewed grounds for optimism as well as some cautionary signals to help guide decision-making in the months ahead.

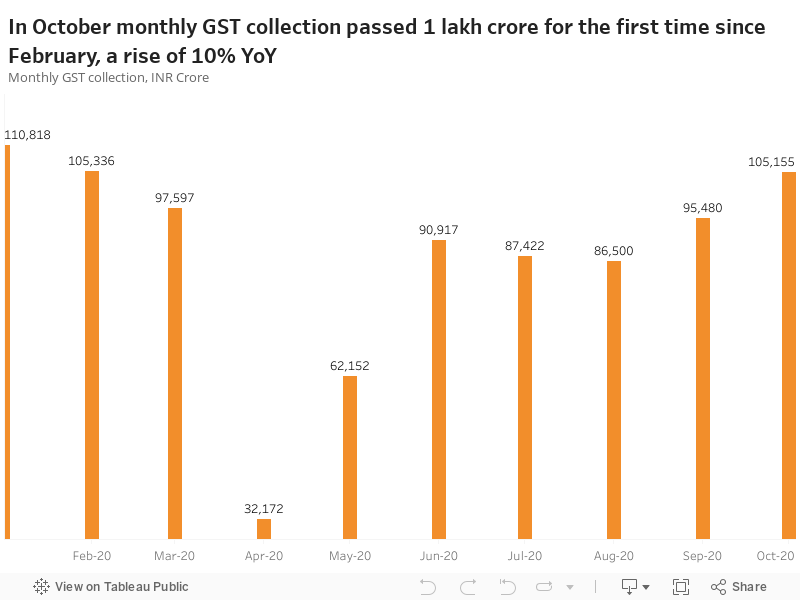

GST collections continue upward trend

In a strong signal of demand recovery, GST collections resumed their upward trend in September and October after stagnating over the summer months. In October total collections surpassed 1 lakh crore for the first time since February, a figure that is 10% higher than the same month last year.